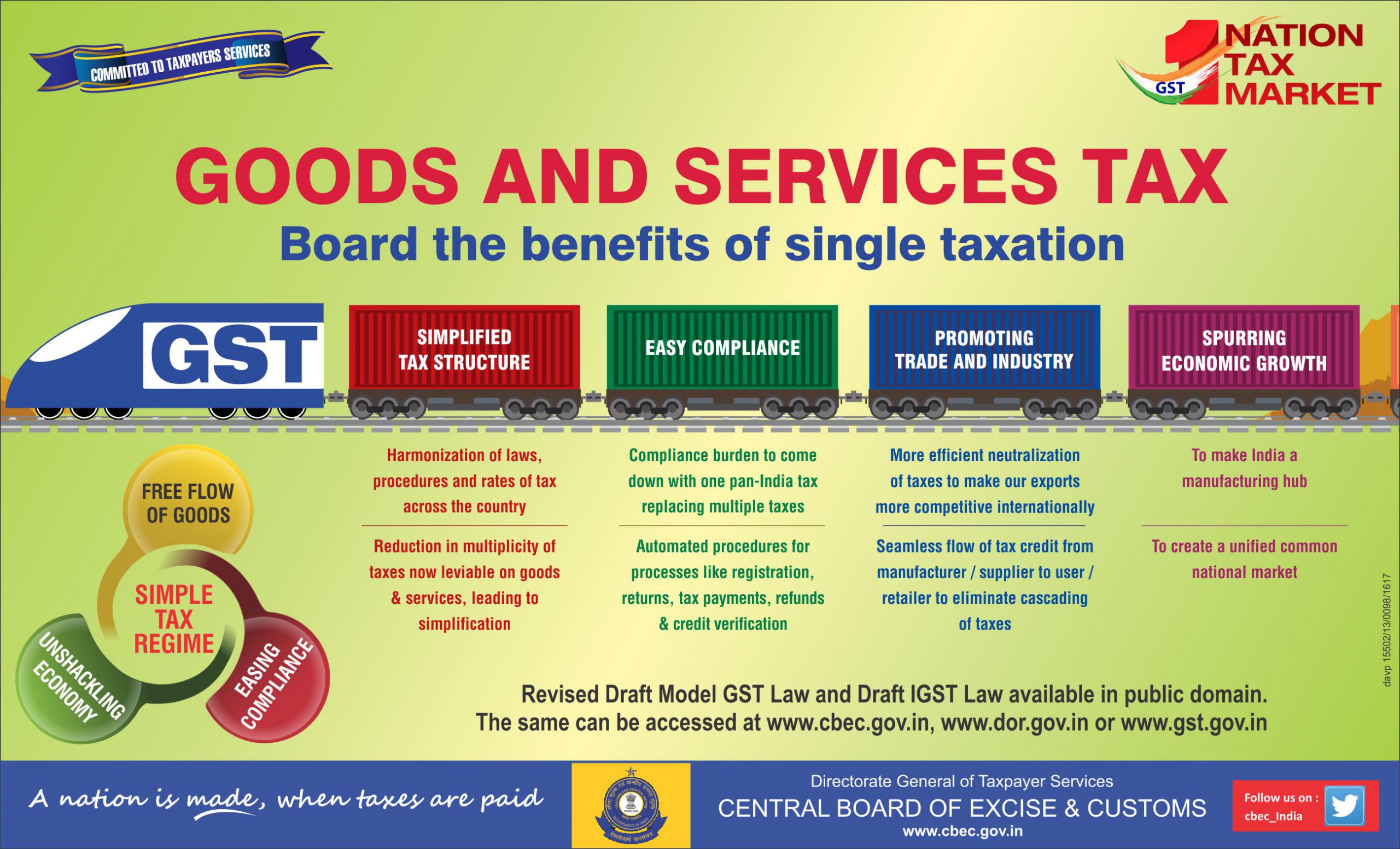

GST is an Indirect Tax which has replaced many Indirect Taxes in India. The Goods and Service Tax Act was passed in the Parliament on 29th March 2017. The Act came into effect on 1st July 2017; Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition.

In simple words, Goods and Service Tax (GST) is an indirect tax levied on the supply of goods and services. This law has replaced many indirect tax laws that previously existed in India.

GST is one indirect tax for the entire country.

GST Registration – Eligibility, Process and Expert Help

GST is the biggest tax reform in India, tremendously improving ease of doing business and increasing the taxpayer base in India by bringing in millions of small businesses in India. By abolishing and subsuming multiple taxes into a single system, tax complexities would be reduced while tax base is increased substantially. Under the new GST regime, all entities involved in buying or selling goods or providing services or both are required to register for GST. Entities without GST registration would not be allowed to collect GST from a customer or claim an input tax credit of GST paid and/or could be penalised. Further, registration under GST is mandatory once an entity crosses the minimum threshold turnover of starts a new business that is expected to cross the prescribed turnover

GST Turnover Limit

There are various types of GST registration and some types of entities like casual taxable persons, non-resident taxable persons or persons supplying through eCommerce operators are required to mandatorily obtain GST registration irrespective of turnover limit. The GST turnover limit for regular GST registration for service providers and goods supplier is provided below.

Service Providers: Any person or entity who provides service of more than Rs.20 lakhs in aggregate turnover in a year is required to obtain GST registration. In special category states, the GST turnover limit for service providers has been fixed at Rs.10 lakhs.

Goods Suppliers: As per notification No.10/2019 any person who is engaged in the exclusive supply of goods whose aggregate turnover crosses Rs.40 lakhs in a year is required to obtain GST registration. To be eligible for the Rs.40 lakhs turnover limit, the supplier must satisfy the following conditions:

- Should not be providing any services.

- The supplier should not be engaged in making intra-state (supplying goods within the same state) supplies in the States of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Puducherry, Sikkim, Telangana, Tripur and Uttarakhand.

- Should not be involved in the supply of ice cream, pan masala or tobacco.

If the above conditions are not met, the supplier of goods would be required to obtain GST registration when the turnover crosses Rs.20 lakhs and Rs.10 lakhs in special category states.

Special Category States: Under GST, the following are listed as special category states – Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand.

Aggregate Turnover: Aggregate turnover = (Taxable supplies + Exempt Supplies + Exports + Inter-State Supplies) – (Taxes + Value of Inward Supplies + Value of Supplies Taxable under Reverse Charge + Value of Non-Taxable Supplies).

Aggregate turnover is calculated based on the PAN. Hence, even if one person has multiple places of business, it must be summed to arrive at the aggregate turnover.

Voluntary GST Registration

Any person or entity irrespective of business turnover can obtain GST registration at any-time. Hence, GST registration is obtained by many businesses in spite of not reaching the aggregate turnover limit. Some of the main reasons for obtaining voluntary GST registration are:

- To improve the business credibility

- To satisfy the requirements of B2B customers

- To claim input tax credit benefits

GST Registration Responsibilities

Entities registered under GST have various responsibilities and compliance requirements from time to time. Failure to comply with the GST regulations or compliance requirements can lead to penalties and revocation of GST registration by the authorities. Some of the main responsibilities of a person registered under GST include:

- Collecting and remitting GST amount from customers

- Issuing proper GST invoice as per the GST rules and regulations

- Filing GST returns whenever due based on turnover – even if there is no turnover or business activity

- FIling annual GST return

- Maintaining all records pertaining to GST for a period of 8 years

We offer a variety of services like income tax filing, GST return filing, private limited company registration, trademark filing and more. We can help you obtain GST registration in India and maintain GST compliance through a proprietary GST accounting software. The average time taken to obtain GST Certificate is about 5 – 10 working days, subject to government processing time and client document submission. Get a free consultation on GST and GST return filing by scheduling an appointment with our advisor.

GST Registration – Documents Required

The following documents must be submitted by regular taxpayers applying for GST registration.

PAN Card of the Business or Applicant

GST registration is linked to the PAN of the business. Hence, PAN must be obtained for the legal entity before applying for GST Registration.

Identity and Address Proof along with Photographs

The following persons are required to submit their identity proof and address proof along with photographs. For identity proof, documents like PAN, passport, driving license, aadhaar card or voters identity card can be submitted. For address proof, documents like passport, driving license, aadhaar card, voters identity card and ration card can be submitted.

- Proprietary Concern – Proprietor

- Partnership Firm / LLP – Managing/Authorized/Designated Partners (personal details of all partners are to be submitted but photos of only ten partners including that of Managing Partner are to be submitted)

- Hindu Undivided Family – Karta

- Company – Managing Director, Directors and the Authorised Person

- Trust – Managing Trustee, Trustees and Authorised Person

- Association of Persons or Body of Individuals –Members of Managing Committee (personal details of all members are to be submitted but photos of only ten members including that of Chairman are to be submitted)

- Local Authority – CEO or his equivalent

- Statutory Body – CEO or his equivalent

- Others – Person(s) in Charge

Business Registration Document

Proof of business registration must be submitted for all types of entities. For proprietorships there is no requirement for submitting this document, as the proprietor and proprietorship are considered the same legal entity.

In case of partnership firm the partnership deed must be submitted. In case of LLP or Company, the incorporation certificate from MCA must be submitted. For other types of entities like society, trust, club, government department or body of individuals, registration certificate can be provided.

Address Proof for Place of Business

For all places of business mentioned in the GST registration application, address proof must be submitted. The following documents are acceptable as address proof for GST registration.

For Own premises

Any document in support of the ownership of the premises like latest Property Tax Receipt or Municipal Khata copy or copy of Electricity Bill.

For Rented or Leased Premises

A copy of the valid rental agreement with any document in support of the ownership of the premises of the Lessor like Latest Property Tax Receipt or Municipal Khata copy or copy of Electricity Bill. If rental agreement or lease deed is not available, then an affidavit to that effect along with any document in support of the possession of the premises like copy of electricity bill is acceptable.

SEZ Premises

If the principal place of business is located in an SEZ or the applicant is an SEZ developer, necessary documents/certificates issued by Government of India are required to be uploaded.

All Other Cases

For all other cases, a copy of the consent letter of the owner of the premises with any document in support of the ownership of the premises of the Consenter like Municipal Khata copy or Electricity Bill copy. For shared properties also, the same documents can be uploaded.

Bank Account Proof

Scanned copy of the first page of bank passbook or the relevant page of bank statement or scanned copy of a cancelled cheque containing name of the Proprietor or Business entity, Bank Account No., MICR, IFSC and Branch details including code.

Reach Us

1007/48, 1st Floor, Above Punjab National Bank,vensor plaza, Dr.Rajkumar Road, Rajajinagar, Bangalore – 560 010

+91 98450 07269 +91 98450 37370 080-2310 6663

info@taxkavach.com